Why do humans live in cities? And why does the urbanization rate of most countries keep increasing? Because there are lots of efficiencies when you put people and companies close together. Goods and services become cheaper and faster to distribute. Electricity, sewage, gas, and other infrastructure services become cheaper and easier to provide. And there are lots of benefits in terms of interactions. Higher population densities enable synergies and lower the unit costs for lots of things. In microeconomics, this is referred to as “economies of density”, which are cost savings resulting from the closer spatial proximity of suppliers and providers. I have discussed this previously, especially when talking about CA10: Location and Transportation Cost and Supply Advantages. In businesses like beer and construction materials, a competitor that is closer to the market can have a cost advantage. Because the transportation cost for the product is a significant percentage of the cost. However, that competitive advantage is available to any company that has a mine or beer bottling facility nearby. This is why beer companies in Bangkok don’t worry about beer companies in Shanghai. It’s mostly a local or regional game on the supply-side. But what about a local beer company with greater volume of sales than another local beer company? That is when we start talking about a scale advantage, not a transportation costs advantage. In this situation, greater customer geographic density can start to become an advantage on the supply-side. This is where economies of scale meets economies of density.

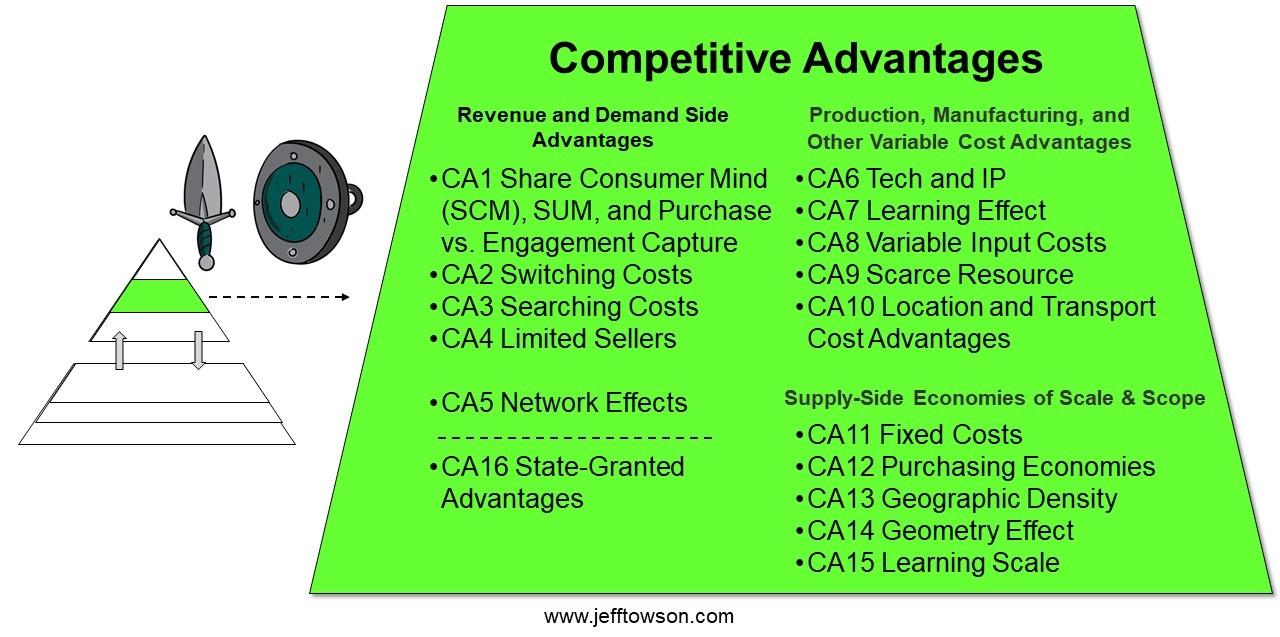

Competitive Advantage 13: Geographic and Distribution Density

A company with more customers within a geographic area will have smaller spatial distances between logistics hubs, distribution points and customers. Think about all the beer and Coca-Cola trucks that are going to convenience stores every day in a city. And all the pizza delivery riders going out to customers. Building scale advantages based on economies of density in distribution has long been a focus of companies like Walmart. As the density of customers and orders within a geographic area increases, the transportation costs can decrease as:

- Utilization at the truck level increases.

- As more distribution nodes are created, which decreases distance.

- As more direct routes can be used.

- And as the overall logistics costs per unit (warehouses plus transportation) decrease.

Geographic density is a competitive advantage that results from having greater customers, volume, nodes, and/or routes within a geographic area than a competitor. For distribution businesses, this can result in:

- Lower costs

- Greater coverage

- Faster distribution times.

Superior geographic and distribution density can be an advantage of the larger players. It’s a scale advantage.  Ok. That was some theory. Let’s look at an example.

Ok. That was some theory. Let’s look at an example.

How Meituan Finally Became Profitable

In 2018, “Amazon of services” company Meituan went public, and I finally got a look at their numbers. Over the previous twelve months, the company had 356M transacting users engaging with 5.1M merchants. The average user did 21 orders per year. Overall, Meituan was averaging +20M daily orders, overwhelmingly in food delivery and restaurant reservations. This was expected as food delivery is typically the first or second most frequently used O2O service on smartphones. For Meituan, food delivery was the primary driver of demand and engagement for their suite of services. CEO Wang Xing had effectively grown that suite of services to include everything from food delivery and hotel reservations to beauty treatments and bicycle rentals. The result was that the company had big users, engagement, and data. These, plus operating cash flow, are the three assets upon which digital platforms are built. But post-IPO, Meituan’s financials were not pretty. The IPO revealed the low profitability of their core food delivery business. Revenue had doubled in 2018 to $4.1B (26B RMB), but gross profits were only 23% and the company had an overall operating loss of 15%. The key numbers in 2018 were:

- Food delivery revenue of $2.5B (16B RMB) with gross profit of 12%. Important: Cost of revenue includes delivery cost.

- Non-delivered services (restaurant reservations, hotels, travel, etc.) generated revenue of $1B (6.8B RMB) with gross profit of 89%.

- Overall, food delivery transactions were 20x hotel reservations by volume. But most profit was from non-delivery services.

It turns out the network effects and other impressive digital strengths of Meituan’s marketplace were not enough to overcome the costs of having tons of people racing all over town on scooters. There was lots of discussion at that time about whether Meituan would ever be economically viable, let alone seriously profitable. This is question still being asked about local mobility services companies like Didi, Lyft and Uber. I was, of course, thinking about the competitive aspects. The company had no big cash engine, despite having a vibrant platform business model in terms of user activity. And its primary competitor was Alibaba, which was targeting all consumer products and services. Really the entire consumer wallet. And in 2018, Alibaba was aggressively going after Meituan’s business via its investee Ele.me. To make matters worse, in the summer of 2018, Alibaba / Ele.me announced a “summer war” against Meituan. They announced they would spend $450M over three months to help Ele.me take market share from Meituan. In practice, this meant lots of user subsidies, payments to logistics personnel and expansion into more segments. At the time, Meituan had 46% of the market compared to 39% for Ele.me, according to consultancy Trustdata. Ele.me was also reported to be raising $2B to continue the fight. Overall, I was not optimistic about Meituan’s prospects. And I ended up being very wrong. Over the next year, Meituan surprised everyone by reaching operating profitability. And, at the same time, expanding its market share significantly versus Ele.me. In the first quarter of 2020, Meituan’s marketshare reached 67%. Ele.me’s market share fell to 27%. Today, Ele.me is still in the game but no longer a serious threat to Meituan. What happened? Well, within Meituan’s 2018 annual report, there was an important comment (added bold is mine): “Our delivery rider cost per order further declined attributable to the continuous expansion of our delivery network, improvement of order density and enhancement of our AI-powered intelligent dispatch system. Our gross margin for food delivery in the first half of 2018 expanded to 12.2% from 9.6% in the same period of 2017.” Note the company’s focus on increasing order density. And on using AI within the distribution operations. Those turned out to be important. As mentioned, in 2019, Meituan surprised virtually everyone by announcing they had achieved positive operating profits. Total annual revenue had grown from 65B to 97B RMB and gross profits had grown from 23% to 33%. This had pulled them to 2% operating profits, despite continued large spending in marketing, R&D, and administration. The key annual numbers for 2019 were:

- Non-delivered services revenue (restaurant reservations, hotels, travel, etc.) had grown 21% with a continued 89% gross profit. These were their most profitable services.

- Food delivery services revenue had grown 43% and had increased gross profit from 12% to 19%.

- Of Meituan’s 17.2B RMB increase in gross profits in 2019, 4.94B came from food delivery. 5.76B came from hotel and 6.5B came from new initiatives.

Here is what they said about their food delivery business in the 2019 annual report (added bold is mine). “As we grow our business, we have also improved the unit economics of our food delivery business on a year-over-year basis consecutively over the past four quarters due to increasing economies of scale.” Note the focus on economies of scale. Running the economies of scale list, we can see two things happening here on the supply-side:

- Meituan is a platform business model and definitely benefits from increasing economies of scale in fixed costs, mostly in IT spending. Unlike Alibaba, this is a digital marketplace with no warehouses. So the continued growth in activity and revenue is going to show up in decreased fixed cost spending per unit. This is CA11: Economies of Scale and Scope in Fixed Costs.

- Meituan also aggressively went after economies of scale in geographic and distribution density, which is the point of this article.

It makes sense if you think about the cost and time for each activity in delivering food orders.

- Riders must go to lots of different restaurants. This is usually within 7-10 kilometers from where they are at that time of receiving an order. But they are going to lots of places.

- They then usually wait while food is being prepared.

- They then pick up one or more orders from that specific restaurant.

- They then go to deliver the order(s) to one or more homes, which can be anywhere within a fairly large radius.

- They sometimes must wait for the customers at the point of delivery.

- Then they accept another order and go to another restaurant,

And that is the simple version. Drivers (cars, motorcycles or scooters) can also pick up orders at other restaurants as they are delivering already picked up orders. Now, think about how these activities change with:

- Increasing customer density in an area.

- Increasing restaurant density in an area.

- Increasing order volume in an area.

In the simplest version, riders are now closer to their next restaurant when they receive an order. The spatial distances decrease with increasing order, restaurant, customer and rider density. But the routes the riders take are not fixed. Riders can change the streets they take to decrease the time to both reach the the restaurant and then the customer. And as riders are usually combining different orders, they can then optimize their routes for that particular order combination. This is why Meituan talked about both increasing density and increasing the use of AI. What we should see with Meituan’s increasing geographic density is:

- Decreasing delivery costs on average.

- Decreasing delivery time.

- Increasing geographic coverage for both customers and restaurants.

All of those are factors that customers and restaurants care about. And that only the market leader will have. It’s a scale advantage. As Meituan achieved more and more orders in a geography (say downtown Shanghai), they increased their geographic density versus ele.me. As the delivery riders fulfilled those orders, the company was able to become more sophisticated in routing riders for both pick-up and delivery. The fleet of riders were algorithmically dispatched to pick-up orders and to take certain routes. Multiple orders could be picked up and delivered along one route by one rider. Riders were also told where to wait for another waiting order. Utilization for both individual riders and for the fleet increased. The average cost per order delivery decreased. Geographic density plus improving AI has turned out to be a real strength for companies like Meituan. Geographic density really works in trucks and scooter delivery. It doesn’t work as well in trains and freight trucks because you can’t alter the routes as much.

Final Point.

This was not the only reason Meituan reached profitability. But I thought it was a good example for geographic density as a competitive advantage. My explanation for how Meituan reached profitability is the following:

- Leaning into geographic density as a scale advantage (as mentioned).

- Withstanding a money war by Alibaba, until they saw it wasn’t working and gave up.

- Aggressively cross-selling between their various services. They shifted users from high engagement services (food delivery) to high margin services (reservations).

- Getting their many new initiatives (bike sharing, ride sharing) to stop losing money.

Cheers, jeff Photo by Taha on Unsplash